A New Plan for American Cities To Free Themselves of Wall Street’s Control

Arbitrary financial fees are sucking cities and states dry. But they can change the terms if they band together and bargain collectively.

Saqib Bhatti

In August 2014, the Los Angeles City Council debated whether to call for the renegotiation of the city’s financial deals. A report by the labor-community coalition Fix L.A. found that the city had spent more than twice as much on banking fees in fiscal year 2013 as it had on street services.

To try to balance its budget, Los Angeles had enacted hundreds of millions of dollars in cuts over the previous five years. City jobs had been slashed by 10 percent, flood control procedures had been cut back, crumbling sidewalks were not repaired and alleys were rarely cleared of debris. Sewer inspections ceased entirely; the number of sewer overflows doubled from 2008 to 2013.

The campaign slogan wrote itself: “Invest in our streets, not Wall Street!”

At the city council debate, Timothy Butcher, a worker with the Bureau of Street Services, got up and said, “I don’t know a whole lot about high finance. I’m just a truck driver. But I do know, if I go to a bank and they give me a bad deal, I don’t deal with that bank any more. And I don’t understand why the city can’t use the same kind of concept on some of these big banks, saying, ‘Hey, help us out or, you know, we’re not going to deal with you any more.’ ”

The City Council approved the resolution unanimously.

It was a blow against both the austerity agenda and the iron grip of Wall Street on American cities. State and local governments in the United States rely on Wall Street firms to put together bond deals, manage their investments and provide financial services. For this, banks charge billions of dollars in fees each year. Public officials believe they have little choice but to cough up. When there are revenue shortfalls, cities typically impose austerity measures and cut essential community services, but Wall Street gets a free pass — payments to banks are considered untouchable.

Public officials assume (wrongly) that financial fees are set in stone because they are based on so-called market rates. However, market rates aren’t preordained by God. Banks set them, and public finance officials simply don’t demand anything substantively lower.

So, what if cities took a page from the labor movement and bargained collectively over interest rates and other financial deals?

The simple reason why anti-union politicians are waging a war on collective bargaining by workers is that it works: There is power in numbers. The basic idea behind such bargaining is to shift the balance of power in the employer-employee relationship and empower workers to negotiate with owners on a more equal footing.

But collective bargaining does not have to be limited to the workplace. Student organizations such as United Students Against Sweatshops have forced university administrations to negotiate over labor standards for their merchandise vendors. Consumer unions press retailers over issues like pricing and safety standards. Community organizations are able to negotiate community-benefit agreements with major corporations in their cities and win benefits such as local hiring policies and community investment standards.

Similarly, public finance officials in cities, states and school districts across the country could apply collective bargaining practices to their financial relationships with Wall Street. While there is no established mechanism for them to do so, there are some creative options worth exploring. For example, cities could establish a nonprofit or publicly funded agency to set guidelines for municipal finance deals and refuse to do business with any bank that does not comply. (More on this later.)

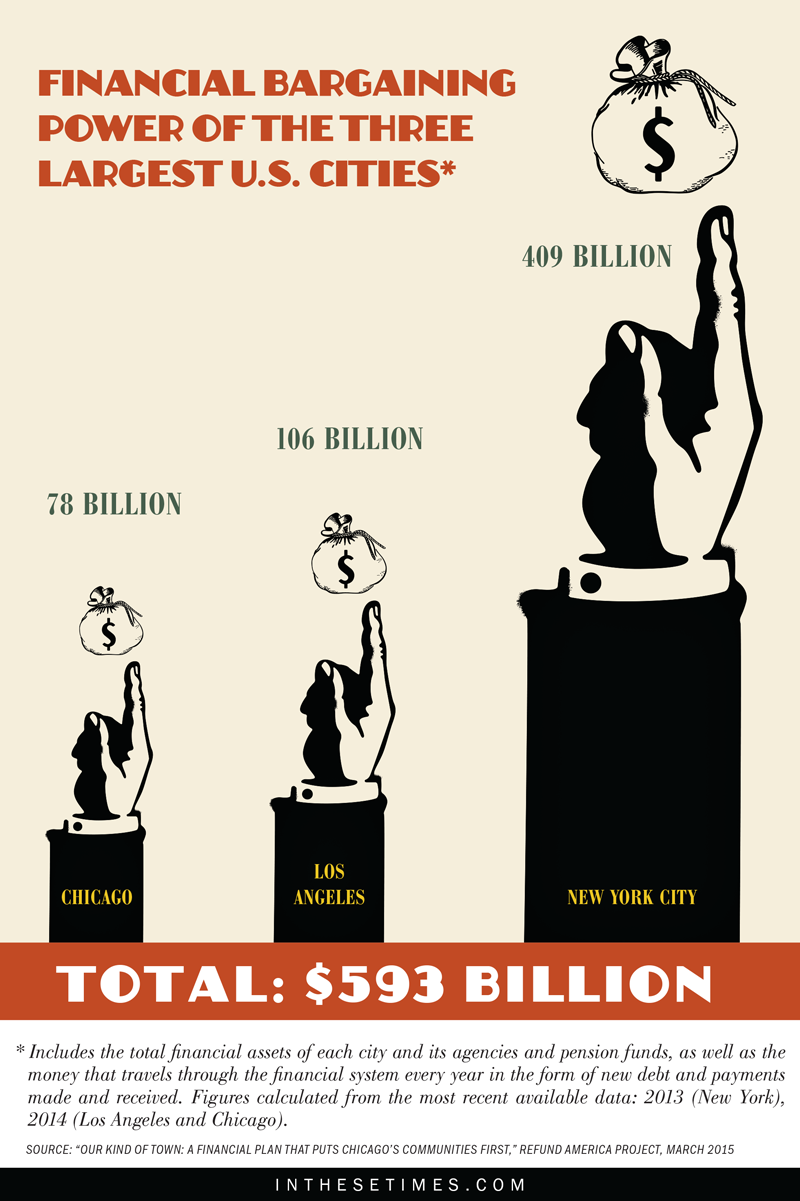

This may sound pie-in-the-sky, but the reality is that American taxpayer dollars are a tremendous source of bargaining power. Just three U.S. cities— New York, Los Angeles and Chicago— together with their related agencies and pension funds, do nearly $600 billion of business with Wall Street every year, more than the gross domestic product of Sweden. Wall Street wants a piece of that action. If it has to jump through a few hoops to get it, it will. This gives public officials the leverage to demand lower interest rates and fairer terms, freeing up scarce funds for community services like parks, libraries and schools.

Runaway fees

Over the last few decades, the banking industry has shifted its profit model away from interest. Big banks’ profits now rely heavily on fees — the money charged for creating loans, packaging them into securities, selling them and servicing them. This structure incentivizes banks to push more complex and expensive deals, like adjustable-rate mortgages and variable-rate bonds, that require fees and add-ons.

Banking fees do not have to bear any relationship to the actual cost of providing services. Banks charge whatever they can get away with, which is why fees have shot up as banks have consolidated and customers’ choices have narrowed. For example, in 2007, Bank of America raised its ATM fee for non-customers from $2 to $3. In all likelihood, the bank’s costs hadn’t suddenly risen 50 percent, despite a spokesperson’s claim that the fee hike would offset “significant” expansion and upgrade of its machines. Banks also arbitrarily raised prices on credit enhancements for municipal borrowers after the financial crash.

For cities and states, which deal in large dollar amounts, this nickel-anddiming hits particularly hard. A 1 percent fee on a $200 million bond is a lot more money than a 1 percent fee on a $200,000 mortgage. That explains why the city of Los Angeles paid $334 million in publicly disclosed fees for financial services in fiscal year 2013, according to the Fix L.A. report. This amount did not include principal or interest on any debt, and neither did it include fees that are not publicly disclosed, like the astronomical fees hedge funds and private equity firms charge pension funds to manage investments.

In Illinois, a preliminary analysis by researchers at the Service Employees International Union (SEIU) — full disclosure: where I used to work — found that the state’s pension funds spent approximately $400 million in publicly disclosed fees in 2014 alone. New York City Comptroller Scott Stringer has released a report showing that nearly all of the returns from the city’s five pension funds over the past 10 years — approximately $2.5 billion — have been eaten up by fees. An investigation by the International Business Times found that New Jersey’s pension funds paid more than $600 million in financial fees in 2014.

Every dollar that banks collect in fees from state and local governments and pension funds is a dollar not going toward essential neighborhood services. It’s not just the streets and sewers of Los Angeles. Illinois is teetering on the edge of a government shutdown. Already, Gov. Bruce Rauner has slashed funding for college scholarships for low-income students, taken a hatchet to vital healthcare programs like Medicaid, and cut state funding for CeaseFire, a highly regarded violence-prevention program with a proven track record.

Most public officials still resist acknowledging that these fees are a problem. When Gov. Rauner tried to cut the municipal share of state income tax revenue by 50 percent this spring, the Illinois House of Representatives responded with a first-of-its-kind resolution urging the state to match any such cuts with proportional cuts to financial-service fees. SEIU also proposed a reduction of financial-service fees during its contract negotiations for state workers, but this was roundly rejected by the Rauner administration.

Of course, Rauner has personally profited from these fees in the past. Before deciding to run for office, he was the managing director of a private equity firm that did business with Illinois pension funds, GTCR LLC.

But even public finance officials who don’t have direct industry ties typically drag their feet on fee reductions. The Los Angeles City Council’s efforts to pressure banks into renegotiating or terminating costly financial deals were met with stiff resistance from the city’s financial officers.

There are a number of reasons why finance staff can be reluctant, if not obstructionist, in efforts to curtail banking fees. One is the revolving door between public finance jobs and Wall Street. Another is the fact that public officials can be outflanked by smoothtalking bankers making dishonest and deceptive sales pitches. But perhaps the biggest reason is that officials truly believe they got the best deal they could. Los Angeles’s finance staff point out that even though they paid $334 million in fees in 2013 alone, they actually did better than many of their peers.

When Councilmember Paul Koretz called for a vote on the motion in Los Angeles, he skewered the City Administrative Officer’s (CAO) office, saying: “Our lack of success in negotiating thus far could partly be a factor of CAO saying that, ‘Hey, this is a fine deal and we’ve done as well on this as anything else we could do.’ ”

Changing the rules

Under the current system, Wall Street sets the rules of the game and public officials think they have no choice but to play on those terms. They may negotiate around the margins and get a fee lowered by half a percentage point, but they do not typically push back on the illogic of the underlying fee structures.

Cities that consider taking a stand against Wall Street are routinely told that if they do, their credit ratings will be downgraded, and banks and investors will stop doing business with them. In reality, the public finance officials who claim they have no choice but to pay high fees and accept onerous terms from Wall Street banks are like elephants afraid of mice. The notion that Wall Street could sustain a prolonged boycott against a city or state as punishment goes against the very nature of banking. U.S. taxpayer dollars are among the largest pools of capital in the world. If there is money to be made, there will always be a bank that will step in to get that business.

Similarly, threats about credit rating downgrades are baseless. Rating agencies are concerned with a borrower’s ability to pay back its bondholders. If anything, negotiating lower fees with banks would free up money and make cities and states less likely to default.

Some cities and states are already blazing the trail. In 2010, then-Massachusetts State Treasurer Timothy Cahill moved state deposits out of Bank of America, Citigroup and Wells Fargo because the banks’ credit card operations did not comply with the state’s usury law, which caps interest rates at 18 percent.

In 2012, the city of Oakland initiated a boycott of Goldman Sachs because the bank refused to renegotiate a deal that had put the city on the losing side of a risky interest-rate bet costing $4 milion in annual fees and payments.

And earlier this year, the Board of Supervisors of Santa Cruz County, Calif., voted not to do any new business for the next five years with banks convicted of felonies. The boycott affects the five banks, including JPMorgan Chase and Citigroup, that pleaded guilty to illegally rigging foreign exchange rates.

These actions are first steps. However, they would be significantly more effective if cities and states joined together. When Oakland — a mid-sized city of 400,000 people — boycotted Goldman Sachs, Goldman didn’t flinch. But if several cities, states and school districts banded together and threatened a boycott, the banking behemoth would be forced to take notice.

Power in numbers

In an ideal world, the federal government would establish standards for protecting state and local officials against predatory financial deals. In the same way that there is a Consumer Financial Protection Bureau, there is a dire need for a Municipal Financial Protection Bureau whose top priority would be to protect taxpayers’ interests. Even though there are already agencies with oversight over municipal finance — such as the Municipal Securities Rulemaking Board and the Securities and Exchange Commission — protecting cities and states from abuse is not their priority. And they have close ties to the financial services industry.

Because federal regulation has proven woefully inadequate, and the chances of effective congressional action in the near future are slim to none, cities and states need to step up.

If just New York, Los Angeles and Chicago banded together and threatened to withhold their collective $600 billion of potential annual business with Wall Street, they wouldn’t have to simply accept the so-called market rates. They have enough bargaining power to set their own.

Together, they could refuse to sign contracts that prevent them from publicly disclosing fees. If they also get their state governments and pension funds on board, they could alter fee structures for things like bond underwriting. They could require any bank that pitches products to sign a fiduciary agreement, meaning they are legally required to put taxpayer interests ahead of their own.

Santa Cruz County Supervisor Ryan Coonerty has already said he is reaching out to other jurisdictions across the country to urge them to join in refusing to do business with felonious banks. If public officials were to coordinate their demands and present a unified front, they could force the banks to take them seriously.

My organization, the Roosevelt Institute’s ReFund America Project, works with community-labor coalitions in cities nationwide that are calling for a reduction in bank fees and an end to predatory municipal finance deals. Last summer, ReFund America and Local Progress — a network linking local elected officials with unions and progressive groups — led a small meeting called “A Progressive Vision for Municipal Finance.” We brought together organizers, policy experts and public officials to discuss various proposals for fixing municipal finance. Among those present were four city councilmembers and three representatives from mayors’ offices. These officials expressed strong interest in developing a bargaining vehicle that would allow cities to take collective action to stand up to Wall Street.

One idea was the creation of a nonprofit or public agency to set municipal finance guidelines. Individual cities and states could subscribe to these guidelines and the agency would in effect become the gatekeeper for banks wishing to do business with them. The more subscribers the agency had, the more bargaining power it would hold. Strict controls would help ensure the agency remained scrupulously independent of Wall Street. That organization could even be the precursor to a national Municipal Financial Protection Bureau.

People over profit

Together, American cities, states and pension funds hold untold power. If they flex their muscles and organize around coordinated demands, they can radically transform taxpayers’ relationship with Wall Street.

In 2012, a community leader from Oakland attended the Goldman Sachs shareholder meeting in New York City and urged CEO Lloyd Blankfein to renegotiate its interest rate swap with the city to avoid library closures and layoffs. He said it was “an issue of morality.” Blankfein responded, “No, I think it’s a matter of shareholder assets.”

This is the mentality that led Rolling Stone’s Matt Taibbi to call Goldman Sachs “a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.”

It’s not just Goldman. All of municipal finance has become an extractive industry, pumping billions away from the communities that need them most. Morality is an externality that financial firms seldom concern themselves with. The financial sector’s fee-based business model is designed to maximize profits, not to protect taxpayers.

Banks may not have a moral compass, but their business contracts with our state and local governments can and should. After all, our cities, states and school districts are not simply fodder for Wall Street’s insatiable greed. Our elected leaders have a duty to protect us from predatory financial practices. Cities and states can force banks to charge drastically lower fees, do away with arbitrary fee structures and eliminate onerous terms that divert billions of dollars away from the most vulnerable members of our society into bonus checks for our nation’s wealthiest few.

Governors in states like Wisconsin, Michigan and Illinois are waging war on collective bargaining and telling taxpayers that empowering publicsector unions robs state coffers, but the real drain on public treasuries is the billions in fees paid to banks every year. And unlike money that goes into workers’ pockets, most of these fees are not recycled back into the local economy but sent to offshore tax havens or invested in complex financial schemes. The irony is that collective bargaining is one of the most effective tools available to public officials who truly want to do right by taxpayers — and cast off Wall Street’s tentacles.

Saqib Bhatti is the Executive Director of the Action Center on Race & The Economy.