"You Are Not A Loan!" Introducing the Nation's First Debtors' Union

Debtors’ unions, in solidarity with labor unions and tenants unions, are the organizing formations we need to dismantle genocidal racial capitalism.

Hannah Appel and Astra Taylor

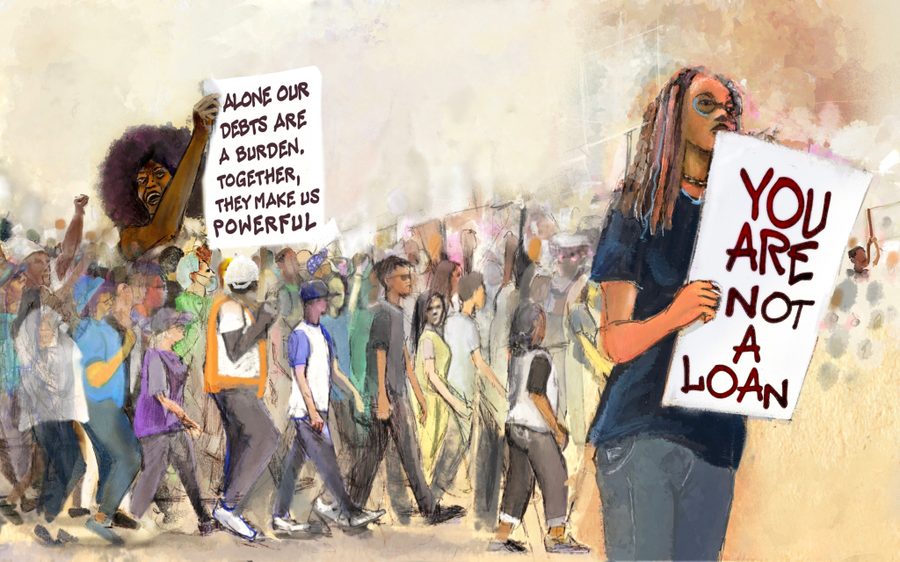

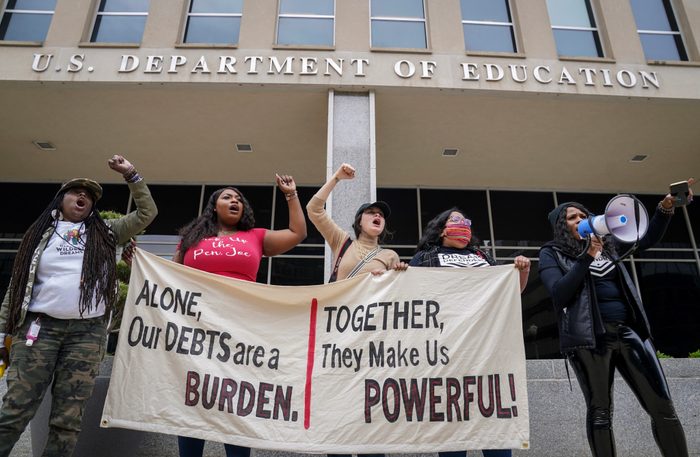

A dozen members of Debt Collective were arrested at a Capitol Hill protest in May demanding that President Joe Biden “fund education, not genocide.” Before they were taken away by police, the protesters unfurled banners reading “You Are Not A Loan” and “$1,700,000,000,000” (the current amount of outstanding student debt).

The connection was clear: Biden can and must use his executive powers to cancel all student debt and fund education, not to authorize and fund Israel’s destruction of Palestine. Organizers and activists came from all over the country to Washington, D.C., to tell him so.

The “Fund Education, Not Genocide” action in May was just a sliver of what we’re about — and what we’re capable of. We’ve been experimenting with building debtor power for more than a decade, and we’ve now secured a previously unthinkable $180 billion in debt abolition for working people across the United States.

We open the special takeover issue of In These Times as two co-founders of Debt Collective — the nation’s first debtors’ union — by welcoming you into our movement and the possibility and promise of debtors’ unions as a new form of collective power.

The writers, organizers, activists, academics and artists in this issue collectively define the landscape of debt in the United States and how deeply it impacts all of our lives. We explore how debt is central to racial capitalism — from how we fund education to how we access medical care; from how we pay for incarceration to how we put a roof over our heads, if we are able.

But we’re not here merely to present household debt as a problem. We’re here with a counterintuitive organizing provocation. At Debt Collective, we believe debt’s ubiquity is a latent form of collective material power and leverage. Rich people already know this. As a quote attributed to famed industrialist J. Paul Getty indicates, “If you owe the bank $100, the bank owns you. If you owe the bank $100 million, you own the bank.”

When debtors get organized in a union formation, we can make good on this insight — together, we own the bank.

We are building a future in which debtors’ unions have the potential to take debt-based housing out of the hands of landlords, banks and mortgage issuers; abolish student debt and force the full funding of public higher education; end medical debt and build the power to finance Medicare for All; abolish carceral debt and build power toward collective liberation.

In other words, we want to introduce debtors’ unions — in solidarity with labor unions and tenants unions — as part of the wall-to-wall counterpower required to dismantle and overcome genocidal racial capitalism, to build the worlds of collective liberation and thriving we need.

The Debt Collective story starts with Occupy Wall Street, in 2011, where we often said that debt is the tie that binds the 99% together. At the time, we didn’t have a clear strategy for how debtors could flex our collective power, but we did know where to start: in the streets.

In 2012, student debt astoundingly hit $1 trillion. We helped mobilize masses into the streets of New York for a “1T Day” protest, demanding not only the wholesale cancellation of student debt, but free college for all.

After our origins at Occupy and our organizing that followed to put the issue of student debt on the map, much of the mainstream press responded with derision about calls to relieve student loans.

Writing for Reuters at the end of 2011, Chadwick Matlin snarked about the prospects of “1T Day” protests: “They want all student debt in the country forgiven. All $1 trillion of it. And if the government would be so kind, they’d appreciate if it would pay for higher education from here on out, as well.”

Larry Abramson, who was then a correspondent for NPR, also lamented in 2011 that “most experts believe there’s little chance the government would ever forgive student loans.”

They didn’t see Debt Collective coming. Today, just over a decade later, our movement has abolished close to $180 billion in student debt, medical debt and carceral debt, and we’ve helped tens of thousands of tenants fight their (often debt-based) evictions in the wake of Covid-19. Student debt is now a key theme in national politics and elections, firmly at the center of both the 2020 and the 2024 presidential primary cycles. In 2023, we brought student debt cancellation all the way to the Supreme Court.

In other words, we’ve changed the game, and we’re just getting started.

We formally launched Debt Collective in 2014. Over the past decade, we have developed not only an understanding of the central role debt plays in our economy and society, but — crucially — the ways our debts can be collectively wielded as a form of power for societal transformation.

Debt bridges the individual and the structural, the personal and political, binding each of us to a broader set of financial and social systems — systems that have emerged over centuries of racist, capitalist and colonialist exploitation and wealth accumulation.

Too often, we experience these racist, patriarchal and classist debts alone, isolated and ashamed.

Black and brown debtors with higher interest rates on everything — from credit cards to mortgages — are told they need more financial literacy, not that our economic system is racist, gendered and broken.

Working people who want to send their kids to college quickly find out their wages can’t cover tuition even at public schools, sending themselves and their kids into a lifetime of debt for a college degree.

Sick people are afraid to go to the hospital because they know they can’t afford the care and already face medical bills they cannot pay.

While housing has become a speculative asset for the wealthy, tenants either cannot move in because rent is too high or their credit score is too low or they are forced to pay a higher security deposit for being poor, for being in debt, for being underpaid, for being Black.

Millions and millions and millions of us are afraid to pick up the phone or open our mail knowing it might be a collection notice, a debt collector, a landlord, a hospital, MOHELA (one outfit that mismanages federal and private student loans on behalf of the U.S. Department of Education and Federal Student Aid) telling us we have to pay a debt — now — that we can’t afford.

But here’s the thing, and it’s why Debt Collective exists: Debtors are not alone and not a loan.

Just as an individual worker is vulnerable without a union, so too with debtors. An individual debtor not paying their debts will see their credit score trashed, wages garnished, access to housing disappeared. But a debtor in a union — organizing with other debtors to negotiate the terms of those credit contracts and the wider capitalist system — has power.

Like workers in a labor union, organized debtors can exercise collective material power over capitalist exploitation. And like labor stoppages, a debt strike — in which debtors withhold payments collectively — is the ultimate threat.

Just as in a labor strike, a successful debt strike requires painstaking, time-intensive organizing, and it’s generally the last tactic, not the first. Day-to-day debtors’ union organizing includes political education, narrative change, community building, innovative legal tactics, policy engagement, protest actions and the slow, steady cultivation of debtor consciousness and effective strategy.

Worker organizing and debtor organizing aren’t merely similar; they complement one another in building anti-capitalist power. Where labor unions often focus on sites of production (the factory floor, the workplace), debtors’ unions focus on circulation (the loan, the credit card, the mortgage) — how and to whom money and capital flow.

Labor organizing primarily targets the employer, demanding higher wages, benefits and more, sometimes bargaining for the common good. Debtor organizing targets the creditor (which, in the era of neoliberalism, is often the state).

Debtor organizing fights against the financialization of life’s basic needs — healthcare, education, housing — and for the universal provision of reparative public goods, so that people don’t have to go into debt to access them.

In our first decade of work at Debt Collective, we’ve spent a lot of time and energy challenging the phony morality and alarming double standards around debt. At the very top of the wealth pyramid, the rules that keep working people in line don’t apply. Companies and the individuals they have made rich walk away from their debts all the time, thanks to bankruptcy laws and government bailouts.

Just look at the 2008 mortgage crisis, when a large percentage of homes in the United States were underwater, meaning the value of the house was less than the mortgage. Homeowners, predictably, did not lose out equally: Black families lost 53% of their collective wealth and Latinx communities 66%, far more than their white counterparts. Quantitative data analysis shows the mortgage crash represented one of the largest destructions of the wealth of people of color in U.S. history.

The same can’t be said for the financiers. By the end of 2008, JPMorgan Chase took $25 billion in bailout cash (transforming public money into private wealth), and executives got massive bonuses.

We watched these double standards play out again during the coronavirus pandemic. While working families waited for paltry stimulus checks, businesses got huge, forgivable loans. Wall Street speculators and billionaires, like Virgin Atlantic founder Richard Branson, lined up at the government trough demanding a handout — and got it. (Branson’s was $1.6 billion.)

Debt Collective believes it is time for debtors to take a page out of the billionaires’ and creditors’ playbook, to see debt and credit for what they are: potential leverage with which to build power for the world we want. Unions of debtors, alongside unions of workers, unions of tenants, powerful abolitionist and environmental justice groups, among others, can and must build the material power to create the world we need.

Debtors’ unions are a new and evolving formation, and we are thinking critically about our adversaries and how best to challenge them: Do debtors’ unions have locals? Are they creditor-based? Are they based on types of debt? Should we organize toward a Wagner Act for debtors — legal protection for debt strikes?

Revolutionary political forms take a long time to establish, and we are just at the beginning of this unprecedented experiment in power-building. World-transforming social movements — abolition, the labor movement, anti-colonial struggle, feminism — grow, build power, change minds, struggle and fight over centuries.

Take the transnational abolition movement. The Haitian Revolution arguably kicked this movement off in 1791, but it was not until 1865 that the 13th Amendment outlawed private chattel slavery in the United States. And of course, the 13th Amendment was not the end of systemic anti-Black racism and white supremacy, but the beginning of a new era of Jim Crow and mass incarceration. Even earth-shattering victories are often the beginnings of new struggles. As one of our movement teachers, Ruth Wilson Gilmore, often puts it, this is why “we must organize for the day after victory.”

Or consider the centuries-long history of the labor movement. Journeymen tailors in New York protested a wage reduction in 1768, a strike that some point to as one of the earliest such walkouts. (Some say that the first dispute that could be labeled a strike took place in Jamestown in 1619 when Polish workers protested being denied the right to vote, while others note a strike in 1786 by journeymen printers.)

The first nationwide strike didn’t happen until more than a century after those brave tailors took action, when more than 100,000 rail workers across the country took part in the Great Railroad Strike of 1877. And not until 1935 did the Wagner Act become law, legalizing and formalizing labor organizing.

Like the 13th Amendment before it, the Wagner Act was only a beginning, with struggles over worker organizing continuing to this day. Revolutionary social movements grow over centuries — we have no choice but to play the long game.

In this issue, we invite you to think of Debt Collective as a version of those journeymen tailors in 1768, experimenting with a new form of solidarity — a kind of solidarity that has radical potential that we are only beginning to understand and unleash. We invite you to think with us, and to join us, as we attempt to lay the groundwork for debtors’ unions.

Get 10 print issues of our award-winning, worker-first journalism here!

HANNAH APPEL is a co-founder of Debt Collective and a professor at UCLA. Her recent publications include Can’t Pay Won’t Pay: The Case for Economic Disobedience and Debt Abolition (coauthored with Debt Collective comrades).

ASTRA TAYLOR is a filmmaker, writer and co-founder of the Debt Collective, a debtors’ union that fights for a democratic, reparative, socialist restructuring of the economy. Her latest book is The Age of Insecurity: Coming Together as Things Fall Apart.