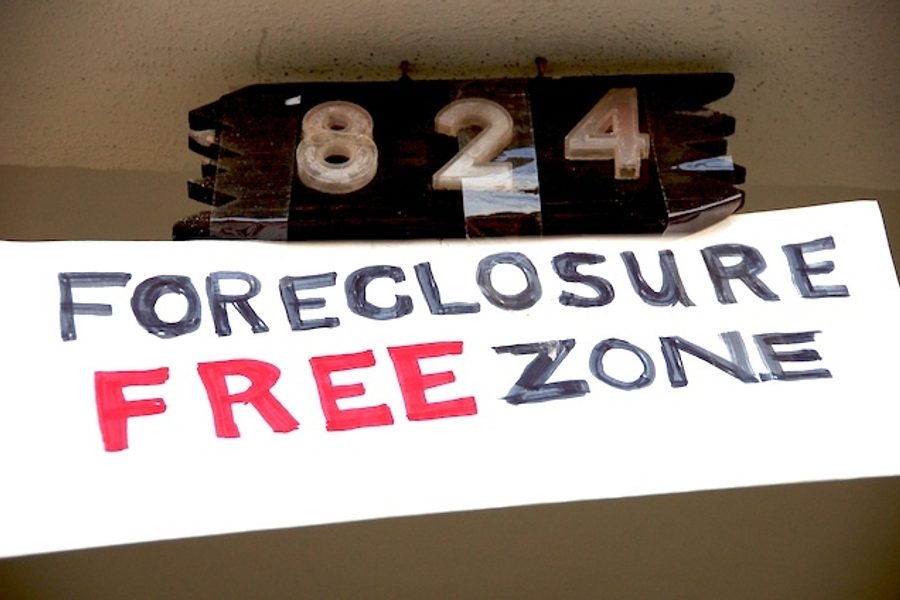

A typical day for a low-income American family begins and ends in uncertainty: getting up in the morning for a job that might be gone tomorrow, and returning at night to a home that might belong to the bank next week.

With foreclosures and job losses engulfing millions of households, the death spiral of negative equity and negative income poses a daunting question for Washington: Can federal housing policy be reoriented away from the intoxicating myth of the “ownership society” — which pumped up the bubble leading up to the housing crash — and toward a vision for economically sustainable communities?

Yet the latest version of Obama’s Home Affordable Modification Program (HAMP) – which has largely failed to stem foreclosures so far – would put a tight squeeze on people scraping by on unemployment benefits. Under the new guidelines, McClatchy reports, “unemployment benefits will no longer count as income for determining whether a person qualifies for a long-term reduction in their mortgage payments… So for people with no income other than unemployment, there will be no loan modifications – the chief tool for preventing foreclosures.”

(HAMP does grant a short-term relief period for unemployed homeowners, though critics say that this, and similar measures in the private sector, are far too short to meet borrowers’ needs).

Aaron Glantz at New America Media reports that foreclosures are now impacting people who had been on relatively safe financial footing — no predatory loan or housing scam — until the recession and job loss threatened to rob them of their home.

Ohio, where foreclosures have accelerated post-industrial urban decay, is a case study. Beth Deutscher, executive director of the Home Ownership Center of Greater Dayton, told the Dayton Daily News that these days, “the people coming to them for help are those who either have lost a job or seen their income drop, not consumers who bought more house than they could afford.”

Among the most blameless victims of the crisis are thousands upon thousands of low-income renters trapped in distressed properties. Even those tenants who always did the right thing, working hard to keep up the rent, may suddenly find themselves paying the price for their landlords’ foreclosure, and then, if they get laid off, bearing the burden of their employers’ troubles.

According to the National Low Income Housing Coalition’s annual report on housing affordability, a family living on the $7.25 minimum hourly wage “would have to work 102 hours each week to afford the nation’s average [fair-market rent] for a two-bedroom home.” (Needless to say, long-term unemployed people who work zero hours a week fare even worse on the “fair market.”)

The foreclosure juggernaut has led housing advocates to demand a more rational approaching to housing policy in Washington — programs based not on the fantasy of the classic suburban fiefdom, but the recognition of everyone’s basic right to a decent home.

The Obama administration has boosted some resources for low-income housing assistance, primarily through Recovery Act provisions like the Homeless Prevention and Rapid Re-Housing Program. The White House’s 2011 budget proposal includes a $350 million program to strengthen public and private rental stock geared toward low-income elderly and people with disabilities.

Yet this relatively bold plan, if enacted, would amount to a mere down payment on the overhaul needed to fill the affordable housing gap. Testifying at a House hearing earlier this month, NLIHC President Sheila Crowley argued that instead of fixating on homeownership, going forward, lawmakers must emphasize rental-ownership balance in expanding housing opportunity.

The NLIHC’s proposed plan centers on a National Housing Trust Fund and massive public investment “to produce, rehabilitate, and/or subsidize at least 3,500,000 units of housing that are affordable and accessible to the lowest income households in the next ten years.”

The Center for Economic Policy and Research sees a more direct way to tie foreclosure relief to affordable rentals: just let distressed borrowers pay rent on their homes until the housing market and the economy stabilize.

And some folks are bypassing Congress altogether. Take Back the Land, a grassroots movement spawned in the midst of Florida’s foreclosure malestrom, is gearing up for a national month of direct actions designed to thwart foreclosures. In several cities, according to the group’s announcement, local activists “will help their family, friends and neighbors ‘live-in’ vacant government owned or foreclosed homes, buildings or land by either moving them in or preventing their eviction.” Not every family can engage in a targeted squatters’ rights movement, obviously, but the protests will expose the absurd irony of foreclosed properties sitting empty while the poor are priced out of the rental market.

In the long run, neither civil disobedience nor foreclosure relief alone would prevent another crisis, absent a dramatic overhaul of the nation’s corrupt housing infrastructure. Advocates say housing policies must invest in comprehensive programs that promote community development, racial and economic inclusion, and social and educational mobility for youth.

The loss of a home isn’t just a setback for an individual household; mass foreclosures undermine property values, exacerbate segregation, erode social cohesion, and generally jeopardize a neighborhood’s future prospects for recovery.

As Roger Bybee pointed out last week, the crisis could be an opportunity for labor to organize workers in communities pummeled by both unemployment and foreclosures. Of course, from a labor standpoint, loan modifications won’t substitute for a comprehensive job-creation program. Still, after so much devastation, working people won’t be able to restore their dignity unless the economy enables them to at least keep a roof over their heads.

Michelle Chen is a contributing writer at In These Times and The Nation, a contributing editor at Dissent and a co-producer of the “Belabored” podcast. She studies history at the CUNY Graduate Center. She tweets at @meeshellchen.