In the 1940s, with the experience of the Great Depression freshly seared into the collective American consciousness, free market economists like Milton Friedman were generally regarded as right wing cranks for believing that government interventions — such as rent control, a minimum wage, even national parks — only got in the way of the market’s superior rationality.

The ideas and policies that dominated economic discourse after the Great Depression were decidedly more left wing. Keynesianism, named after its leading theoretician John Maynard Keynes, emphasized an active borrow-and-spend role for government to maintain full employment and keep the economy humming. But within a few decades, conservative economics gained political hegemony. Friedman himself won the Nobel Prize in economics in 1976, and advised or influenced a global who’s who of right wing leaders, from Ronald Reagan to Margaret Thatcher to Augusto Pinochet. And the ideas of the Chicago school, as Friedman’s brand of economics came to be known, now dominate the current response to the inflationary crisis.

In Friedman’s view, Keynesian deficit spending pushes the Federal Reserve to expand the money supply, which inevitably leads to “too much money” chasing “not enough goods” — and consumers then bid against each other, driving up prices.

The full (or high) employment sought by Keynesians exacerbates inflation, the argument goes. Workers, insufficiently afraid of losing their jobs in a flush economy, demand higher wages. Businesses then pass off labor costs to consumers by further hiking prices — and the result is an inflationary cycle, as the prices of goods and labor both rise. Thus inflation must be fought by constricting the money supply, pulling back government spending and actually increasing unemployment, to curb workers’ bargaining power.

But behind these technical economic arguments lies a political, class-war principle. Why must business owners pass off rising costs to consumers through price hikes, after all? If wages went up and prices were to stay the same, that simply means a greater share of profits would go to workers rather than capitalists. Inflation, therefore, is a site of class conflict — a battle of which class is gaining at the other’s expense.

Right now, the corporate class is happily gaining. Many corporations are seeing sky-high profits. The Wall Street Journal reports that S&P 500 companies have raised prices about 20% higher than the rate of inflation of wholesale goods — meaning they are adding a fat profit margin beyond their increased costs. In fact, corporate profits at nonfinancial companies account for more than half of recent price growth, according to the progressive Economic Policy Institute.

The Biden administration, at the prompting of progressive economic groups, has laid some blame for inflation at the feet of corporations, calling out the monopolistic meatpacking industry for price gouging, for example, and the oil industry for holding back on production to keep profits high. “Exxon made more money than God this year,” the president said in June.

Yet conservative economic theory, like that trumpeted by Friedman, still drives the story we hear repeated ad nauseam in mainstream discussions of inflation: increased wages and government spending are to blame. Only the Federal Reserve can beat inflation by “cooling” the economy. The government’s only role is to refrain from substantive spending.

Biden could have invoked executive powers to institute targeted price controls and invest in production, but he didn’t. Instead, the Federal Reserve is hiking interest rates, and the administration’s landmark social spending bill, Build Back Better, got whittled down and reframed into the Inflation Reduction Act, which includes some positive gains (like corporate taxes and reduced drug prices) but operates within the confines of conservative monetary justifications.

To articulate and fight for an alternative solution to inflation, we need to radically shift the economic discourse to the left.

WHAT THE RULING CLASS LEARNED IN THE ‘70S

Milton Friedman said in 1982 that you need “ideas that are lying around,” until a crisis arises when “the politically impossible becomes the politically inevitable.” For Friedman, that opportunity came in the form of a “stagflation” recession (so-called for combining high rates of inflation with stagnant economic growth) in the 1970s. The spiraling inflationary crisis and its eventual resolution through drastic monetary tightening seemed to vindicate Friedman’s ideas. Keynesian economic policy was definitively replaced by a conservative economic orthodoxy.

The 1970s proved to be a pivot of economic eras in the United States as the postwar Golden Age boom came to an end. U.S. factories faced competitive pressure from Western Europe and Japan; an oil embargo from Arab members of OPEC contributed to skyrocketing energy costs; and a militant labor movement at home successfully fought for higher wages and greater control on the shop floor, ensuring wage growth outpaced productivity gains. As corporate manufacturing profits shrank, American capitalists responded by hiking prices. In doing so, they unleashed an inflationary spiral.

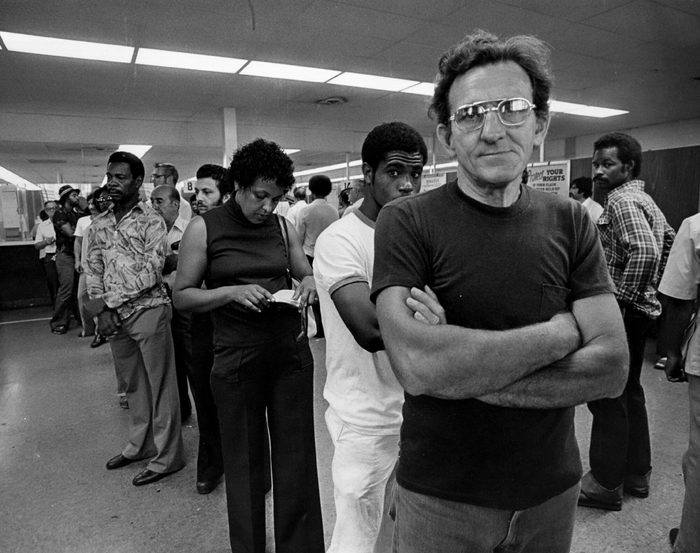

In what came to be known as the “Volcker shock,” then Federal Reserve Chair Paul Volcker engineered an unprecedented hike in interest rates. Higher rates slowed investment and shuttered many businesses, which lowered consumer demand and triggered massive unemployment. That unemployment was not an accident — Volcker intended to break workers’ confidence so they would not demand higher wages. Meanwhile, the Reagan White House did its part by firing more than 11,000 striking air traffic controllers in 1981, making it clear which side of the class struggle the government was on.

Mass unemployment — which peaked at 10.8% in 1982, the highest since the Great Depression — and the fear of losing their jobs scared millions of workers into a submissive posture. As economic historian Tim Barker described for the magazine n+1, the Volcker shock turned the industrial belt into the Rust Belt:

In places like Flint, Michigan and Youngstown, Ohio, more than one in five workers were unemployed. In Akron, the commercial blood bank reduced the prices it would pay by 20% due to the glut of laid-off tire workers lining up to bleed. In the area around Pittsburgh, suicide rates and alcoholism soared, while residents competed for spots in homeless shelters. The unemployment rates for African Americans were worse, peaking in early 1983 at 21.2%.

Manufacturing jobs had been a key source of unionization, and union density declined precipitously throughout the 1980s, falling from 23% to 16% by the decade’s end — and it has been falling ever since.

The American ruling class has since won ever higher labor productivity and profit rates. Workers keep working harder for less. Friedman’s ideas provided a seemingly technical and apolitical cover for the restoration of capitalist profitability at the expense of the working class.

The Fed seemed to take a more dovish turn this past decade, allowing the economy to expand despite low unemployment rates. And, by lowering the cost of government debt, it made possible the pandemic-era deficit-driven social spending. But, as Barker has argued, low interest rates were only allowed in so far as they didn’t risk inflation — a risk that was forestalled by a weak labor movement that did not press wage demands, even when unemployment dropped below 5% in 2016.

As the economy expanded, it largely added non-union, poorly paid jobs. “The current experiment,” Barker explained, “was made possible by a recognition that workers had suffered a secular defeat — specifically, that they had lost the ability to increase or even defend their share of the national income.”

TODAY’S CRISIS

For a brief moment last year, the scale of the economic crisis wrought by the pandemic looked like it might force a more dovish economic approach from the American ruling class. The government ramped up deficit fueled stimulus spending. The Federal Reserve kept the spigot of cheap cash flowing. Poverty levels actually dropped in the midst of a severe economic crisis, and the wide chasm of U.S. income inequality narrowed ever so slightly.

Early in 2021, when the prospect of inflation first reared its head, talk of rolling back government stimulus was still an outlier position. Neoliberal economist Larry Summers returned from hibernation to argue against giving too much help to struggling households. But for a blissful moment, his arguments were confined to a few dissident editorials, seemingly ignored by those in power. Federal Reserve Chair Jerome Powell argued that rising prices were a short-term, transitory problem because of supply chain shocks and the pandemic.

But inflation has stubbornly stuck around, propelled by a number of factors. Thin inventories motivated by just-in-time production methods made it difficult to meet growing demand. Russia’s invasion of Ukraine contributed to high oil prices, which impact almost every part of the economy. Pandemic-era benefits modestly fueled demand by putting more money in circulation. And company CEOs took advantage of the increased demand and engaged in price gouging, raising prices much higher than their supply costs.

To say rising wages are playing a role in inflation however — as they did in the 1970s — is a stretch. According to the Bureau of Labor Statistics, real wages (adjusting for inflation) were actually 3% lower this July than last. The failure of wages to keep up with prices is causing real economic pain. All the more so because lower-income households— which are disproportionately households of color — spend at least three-quarters of their income on necessities.

Nevertheless, corporations are fearful that the tight labor market will eventually cause wages to rise. A June Bank of America memo, obtained by The Intercept, bemoaned that it will “be hard to reverse” tight labor conditions and upward wage pressures. For workers, that would be good news, as the effects of inflation would be offset by higher wages. To those in charge of fiscal policy, however, controlling inflation (largely to the benefit of business) is considered more important than maintaining low unemployment (to the benefit of workers).

As inflation rose this year, Powell and the Fed shifted into inflation-fighting mode. Since March, they’ve raised interest rates five times, the highest sixth-month increase in over 40 years. Three more increases this year are considered likely. So far, these actions fall well short of a Volcker shock, but Powell has repeatedly stressed the Fed will continue to raise rates until inflation is under control — even if that means causing a recession and high unemployment. Speaking at the European Central Bank’s conference, Powell said, “Is there a risk we would go too far? Certainly, there’s a risk. … The bigger mistake to make — let’s put it that way — would be to fail to restore price stability.” He added: “The process is highly likely to involve some pain, but the worse pain would be in failing to address this high inflation.”

Summers is more explicit about the effect of the Fed’s policies. “I don’t see how we can get inflation to substantially decelerate without wage inflation falling substantially,” he told the Washington Post, “and I don’t see any reason to think wage inflation will fall substantially unless there’s a substantial loosening in labor markets, which would mean higher unemployment.” Never mind that “wage inflation” is arguably nonexistent; Summers prescribes either five years of unemployment above 5%, or one year above 10%.

That would soothe the fears of the capitalist class. Whether or not wages contribute to inflation, a slack labor market remains a priority for American capitalists because of the precedent that increased workers’ bargaining power could portend. A tight labor market opens the way to greater gains and organizing efforts for workers (like this year’s wave of Starbucks union drives). As the uncovered Bank of America memo says, “By the end of next year, we hope the ratio of job openings to unemployed is down to the more normal highs of the last business cycle.”

The Fed is on track to deliver on that hope.

A LEFT RESPONSE

Karl Marx argued that capitalism depends on unemployment — a “reserve army of labor” — to keep workers desperate enough to agree to whatever work they get. Unemployment, in other words, plays a critical role in capitalism, preventing wage growth from threatening profitability.

By definition, capitalism holds us hostage to the market’s profit motive. Even in “good times,” the consequences are dire — as investment flows toward fossil fuels rather than ecological sustainability, for example, or toward pharmaceutical windfalls rather than equitable vaccination distribution. But in bad times, our lives are thrown into chaos and despair, subjected as we are to the whims and impacts of supply and demand.

Capitalism cyclically falls into crises of inflation and recession, and as another wave hits, the Federal Reserve and the White House are determined to force working people to carry the burden through layoffs, diminished wages and an inadequate social safety net. If capitalist profits were on the hook instead (by taxing the rich and corporations, say, or through targeted price controls), then pro-worker policies could be put into place (such as lowering the social costs of childcare, housing and healthcare).

Such reforms have long been on the ready. Rent control policies, for instance, were first introduced nationally as part of President Franklin D. Roosevelt’s Emergency Price Control Act in 1942. Expanding Medicare has been at the heart of the Bernie Sanders Left for years. And public investment in housing, transportation and education would go a long way toward reducing working-class people’s daily expenses.

Higher taxes would simultaneously reduce the government deficit (the bête noire of the monetarists) and reduce inequality. The Inflation Reduction Act does take this approach, with a 15% corporate minimum tax that nullifies tax loopholes and a 1% tax on stock repurchases, targeting companies reaping the biggest profits from inflation. A proposal by Sen. Bernie Sanders would have done so more effectively, by taxing at 95% the profits of companies making more than they did before Covid-19.

Price controls are less familiar to today’s progressive movement, but, in fact, they are a necessary response to the realities of the “free market.” There is nothing “natural” or “fair” about the market determining prices — especially because sellers simply “pick their price” in a market that’s in short supply (economists’ sterile description of “price gouging”).

And price controls have actually been used throughout U.S. history. As political scientist Todd Tucker pointed out, FDR employed 160,000 federal employees in the Office of Price Administration to control prices “on goods from scrap steel to shoes to milk.” Even President Richard Nixon briefly implemented price controls. Most recently, the U.S. government’s provision of free Covid vaccines was a form of price control, as the state directly negotiated prices.

Most immediately, capping the prices of energy and fuel would protect working people’s pockets and reduce production costs for businesses across the economy. Of course, such measures would make a dent in the oil industry’s profits — but this should be seen as part of a longer-term strategy to transition away from fossil fuels. Another immediate course would be to pursue aggressive anti-trust measures, which would help tame the price-setting powers of monopolies.

In arenas where the federal government has significant economic authority, such as healthcare and higher education, this authority should be wielded to drive down prices. As the Left has long argued, allowing Medicare to negotiate fair prices for prescription drugs would lower costs dramatically, as private prices tend to follow Medicare’s lead. Federal funding for higher education, which accounts for about 14% of college revenue, could be tied to caps on tuition increases.

Alongside state intervention to control rising costs, the government could play a greater role in untangling supply chain chokeholds. Higher interest rates will not, in fact, increase the productive capacity for things like cars or baby formula. On the contrary, they may act as an impediment to greater investment in productive capacity. The government could instead invoke the Defense Production Act to support investments in the production of targeted goods, such as semiconductors and housing construction inputs (which have played outsized roles in supply-chain chokeholds), and to invest in green energy production.

All of these examples would provide considerable relief to inflationary pressures — while laying the groundwork for a more democratic control of the economy long term.

In the 1970s, a strong labor movement meant even the historic rates of inflation hurt capital more than they did workers, as sociologists Ho-fung Hung and Daniel Thompson have argued. High wages and welfare benefits tied to price hikes mitigated the effects on workers, and income inequality dropped to its lowest level in the postwar era. This balance of forces is precisely what the ruling class worked to reverse through the Volcker shock and the offensive against the labor movement.

Neoclassical economic philosophy provided both a technical tool and a political cover for the American ruling class to roll back the gains of the New Deal and the postwar boom. The past four decades of neoliberal rule have been their victory dance.

The Left urgently needs an answer to inflation. In the short term, we need to articulate and organize for an economic agenda that mitigates the effects of the crisis for working people by taxing the rich, controlling prices and socializing major expenses. Critically, we need to back labor organizing that pushes for higher wages, and reject narratives that “too high” wages are a problem.

In the long term — recognizing that capitalism is an inherently unstable system that resolves its crises on the backs of working people — a left economic agenda needs to frame a vision for a different kind of economy, one based on human need rather than corporate profit. Right now, even minor advances in working-class living standards result in devastating economic lurches. How can a system be defended if it goes into crisis at the very prospect of slight wage increases? Or in response to a government bailout of the unemployed during a pandemic? Is the current system really the best we can do?

Hadas Thier is an activist and socialist in New York, the author of A People’s Guide to Capitalism: An Introduction to Marxist Economics, and a regular contributor to Jacobin Magazine. She tweets at @HadasThier.